Sequential restoration regardless of a difficult world atmosphere Operating efficiency above our estimates

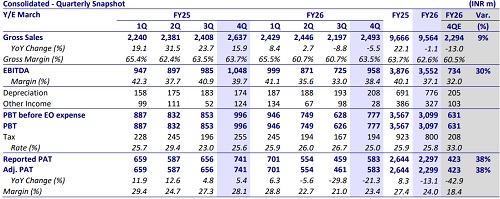

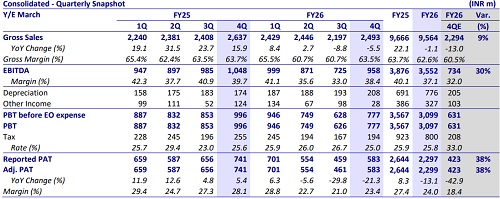

* Clean Science (CLEAN) reported an EBITDA of INR958m, down 9% YoY, whereas its gross margin dipped marginally to 63.5% (from 63.7% in 4QFY25). The EBITDA margin contracted to 38.4% (from ~39.7% in 4QFY25).

* FY26 was marked by a difficult world macro atmosphere and geopolitical uncertainties, resulting in subdued buyer offtake and pricing stress. We count on CLEAN’s earnings trajectory to maneuver up because of its continued concentrate on course of effectivity, backward integration, scale up of Hindered Amine Light Stabilizers(HALs), and the ramp up of efficiency chemical 1, together with the commercialization of efficiency chemical 2 in Sep’26E.

* We elevate our earnings estimates for FY27/FY28 by 6% every and worth the inventory at 25x FY28E EPS to reach at our TP of INR840. Reiterate Neutral.

Weak efficiency chemical substances offset development in pharma intermediates and FMCG

* The firm reported a income of INR2.5b, down 5% YoY (est. INR2.3b), whereas income for Pharma & Agro Intermediates/FMCG Chemicals grew ~8%/~49% YoY to INR615m/INR366m. The income for efficiency chemical substances (~61% of the income in 4Q) declined ~17% YoY to INR1.5b.

* Gross margin stood at 63.5% (in comparison with 63.7% in 4QFY25 ), whereas EBITDA margin stood at 38.4% (in comparison with 39.7% in 4QFY25)

* Employee exp as % gross sales stood at 2% (in comparison with 6% in 4QFY25) as the government Directors voluntarily elected to forgo a considerable portion of their efficiency bonus entitlement for the FY25-FY26. Accordingly, the provision for efficiency bonus acknowledged in the earlier quarters has been reversed to that extent, leading to decrease worker advantages expense in 4Q.

* EBITDA declined 9% YoY to INR958m, above our estimate of INR734m. Based on the assumption of normalized worker prices (the common of the final three quarters), adj. EBITDA declined ~19% YoY to INR850m.

* Adj. PAT stood at INR583m (down 21% YoY) in 4QFY26 (est. INR423m).

* In FY26, income /EBITDA/Adj. PAT declined 1%/8%/13% to INR9.6b/ INR3.6b/INR2.3b

Valuation and look at

* While the macro headwinds are anticipated to proceed in the quick time period,

1) the ramp-up of the superior grade HALs

2) strengthening HALs’ presence in valueadded specialty chemistries

3) the scale-up of efficiency chemical 1 together with the commercialization of efficiency chemical 2

4) backward integration initiatives are anticipated to be key development drivers going ahead.

* We elevate our earnings estimates for FY27/FY28 by 6% every and count on a CAGR of 21%/21%/25% in income/EBITDA/ PAT over FY26-28. We worth the inventory at 25x FY28E EPS to reach at our TP of INR840. Reiterate Neutral.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration quantity is INH000000412