Key Insights

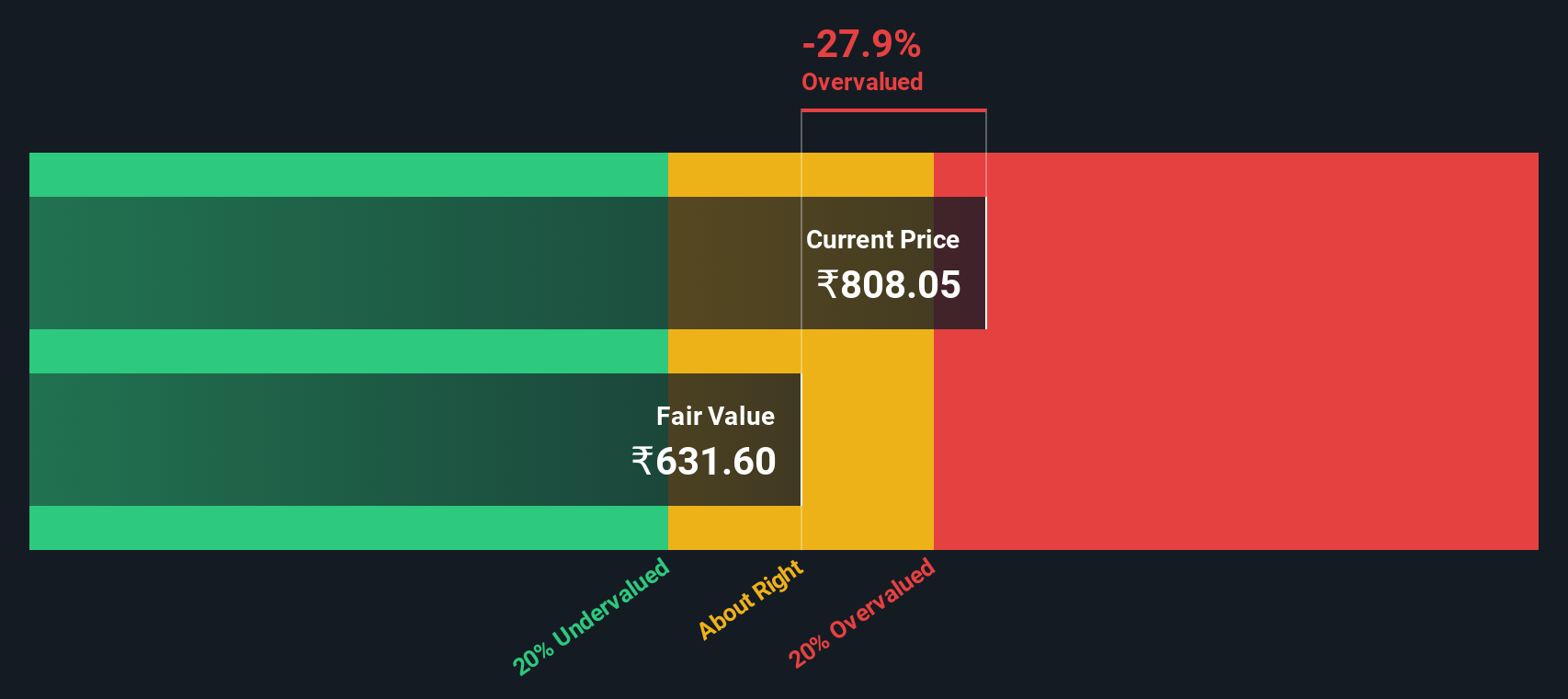

- The projected truthful worth for Clean Science and Technology is ₹632 based mostly on 2 Stage Free Cash Flow to Equity

- Current share value of ₹808 suggests Clean Science and Technology is probably 28% overvalued

- Analyst price target for CLEAN is ₹1,140, which is 80% above our truthful worth estimate

Does the February share value for Clean Science and Technology Limited (NSE:CLEAN) mirror what it is actually price? Today, we are going to estimate the inventory’s intrinsic worth by taking the anticipated future money flows and discounting them to in the present day’s worth. We will use the Discounted Cash Flow (DCF) mannequin on this event. Models like these might seem past the comprehension of a lay individual, however they’re pretty simple to comply with.

Companies could be valued in a variety of methods, so we might level out {that a} DCF isn’t excellent for each scenario. Anyone desirous about studying a bit extra about intrinsic worth ought to have a learn of the Simply Wall St analysis model.

The Calculation

We are going to make use of a two-stage DCF mannequin, which, because the title states, takes under consideration two levels of progress. The first stage is mostly the next progress interval which ranges off heading in the direction of the terminal worth, captured within the second ‘regular progress’ interval. In the primary stage we have to estimate the money flows to the enterprise over the following ten years. Where doable we use analyst estimates, however when these aren’t obtainable we extrapolate the earlier free money movement (FCF) from the final estimate or reported worth. We assume firms with shrinking free money movement will sluggish their charge of shrinkage, and that firms with rising free money movement will see their progress charge sluggish, over this era. We do that to mirror that progress tends to sluggish extra within the early years than it does in later years.

Generally we assume {that a} greenback in the present day is extra helpful than a greenback sooner or later, and so the sum of those future money flows is then discounted to in the present day’s worth:

10-year free money movement (FCF) forecast

(“Est” = FCF progress charge estimated by Simply Wall St)

Present Value of 10-year Cash Flow (PVCF) = ₹22b

We now have to calculate the Terminal Value, which accounts for all the long run money flows after this ten 12 months interval. The Gordon Growth formulation is used to calculate Terminal Value at a future annual progress charge equal to the 5-year common of the 10-year authorities bond yield of 6.8%. We low cost the terminal money flows to in the present day’s worth at a value of fairness of 13%.

Terminal Value (TV)= FCF2035 × (1 + g) ÷ (r – g) = ₹9.8b× (1 + 6.8%) ÷ (13%– 6.8%) = ₹159b

Present Value of Terminal Value (PVTV)= TV / (1 + r)10= ₹159b÷ ( 1 + 13%)10= ₹45b

The whole worth, or fairness worth, is then the sum of the current worth of the long run money flows, which on this case is ₹67b. To get the intrinsic worth per share, we divide this by the full variety of shares excellent. Relative to the present share value of ₹808, the corporate seems barely overvalued on the time of writing. Valuations are imprecise devices although, slightly like a telescope – transfer a number of levels and find yourself in a distinct galaxy. Do maintain this in thoughts.

Important Assumptions

Now an important inputs to a reduced money movement are the low cost charge, and after all, the precise money flows. If you do not agree with these consequence, have a go on the calculation your self and play with the assumptions. The DCF additionally doesn’t think about the doable cyclicality of an business, or an organization’s future capital necessities, so it doesn’t give a full image of an organization’s potential efficiency. Given that we’re Clean Science and Technology as potential shareholders, the price of fairness is used because the low cost charge, slightly than the price of capital (or weighted common value of capital, WACC) which accounts for debt. In this calculation we have used 13%, which relies on a levered beta of 0.888. Beta is a measure of a inventory’s volatility, in comparison with the market as an entire. We get our beta from the business common beta of worldwide comparable firms, with an imposed restrict between 0.8 and 2.0, which is an inexpensive vary for a steady enterprise.

See our latest analysis for Clean Science and Technology

SWOT Analysis for Clean Science and Technology

- Dividends are coated by earnings and money flows.

- Earnings declined over the previous 12 months.

- Dividend is low in comparison with the highest 25% of dividend payers within the Chemicals market.

- Expensive based mostly on P/E ratio and estimated truthful worth.

- Annual earnings are forecast to develop quicker than the Indian market.

- No obvious threats seen for CLEAN.

Next Steps:

Although the valuation of an organization is essential, it should not be the one metric you have a look at when researching an organization. DCF fashions usually are not the be-all and end-all of funding valuation. Instead the perfect use for a DCF mannequin is to check sure assumptions and theories to see if they’d result in the corporate being undervalued or overvalued. For instance, modifications within the firm’s value of fairness or the chance free charge can considerably affect the valuation. Can we work out why the corporate is buying and selling at a premium to intrinsic worth? For Clean Science and Technology, we have compiled three pertinent components it’s best to have a look at:

- Risks: For instance, we have found 1 warning sign for Clean Science and Technology that try to be conscious of earlier than investing right here.

- Future Earnings: How does CLEAN’s progress charge examine to its friends and the broader market? Dig deeper into the analyst consensus quantity for the upcoming years by interacting with our free analyst growth expectation chart.

- Other High Quality Alternatives: Do you want a superb all-rounder? Explore our interactive list of high quality stocks to get an concept of what else is on the market chances are you’ll be lacking!

PS. Simply Wall St updates its DCF calculation for each Indian inventory every single day, so if you wish to discover the intrinsic worth of some other inventory simply search here.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every single day to uncover alternatives.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High progress Tech and AI Companies

Or construct your individual from over 50 metrics.

Have suggestions on this text? Concerned in regards to the content material? Get in touch with us instantly. Alternatively, e-mail editorial-team (at) simplywallst.com.

This article by Simply Wall St is normal in nature. We present commentary based mostly on historic knowledge and analyst forecasts solely utilizing an unbiased methodology and our articles usually are not supposed to be monetary recommendation. It doesn’t represent a advice to purchase or promote any inventory, and doesn’t take account of your aims, or your monetary scenario. We goal to carry you long-term centered evaluation pushed by basic knowledge. Note that our evaluation might not issue within the newest price-sensitive firm bulletins or qualitative materials. Simply Wall St has no place in any shares talked about.